2025/4/22

I.Production & Inventory

In 2024, China’s chemical fiber industry load was relatively high; overall performance was higher than 2023. In particular, the average capacity utilization rate of direct-spun polyester filament and civilian polyamide filament was more than 90%, 7.8 and 8.8 percentage points higher than that of 2023, respectively. By staged view, in the March-April period, downstream demand performed better than expected, with the capacity utilization rate of most of the chemical fiber sub-industries maintained at a high level in the same period in recent years. But that also caused the accumulation of inventories, narrowed benefits, coupled with entering the off-season, part of the polyester enterprises even faced losses. In the June-August period, the polyester capacity utilization rate declined, and then recovered slightly in September. In the fourth quarter, it maintained a high level of operation.

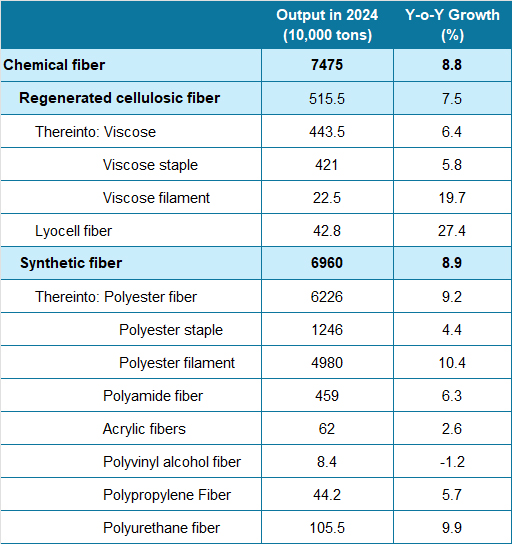

With a high capacity base and high capacity utilization rate, chemical fiber output grew faster in 2024. According to the China Chemical Fibers Association, chemical fiber output in 2024 totaled 74.75 million tons, up 8.8% year-on-year (Table 1).

Table 1: China’s Chemical Fiber Output in 2024

Note: The above statistics include recycled fibers and do not include post-processing products such as textured yarn.

Source: China Chemical Fibers Association

II.Terminal Demand

In 2024, a timely package of policies aimed at promoting social confidence effectively boosted the economy, leading to moderate growth in domestic sales of textiles and apparel. Regarding external demand, the competitiveness of China’s textile industry chain continually improved, successfully withstanding the more challenging foreign trade situation, and exports throughout the year experienced growth.

From the downstream of chemical fibers, the output of chemical fiber yarn and chemical staple fabric increased by 8.2% and 3.4% year-on-year. Meanwhile, the operating rate in the downstream sector of the major chemical fiber industry, including texturing, improved compared to 2023. From the perspective of textile city turnover, the average value was slightly lower than in 2023.

III. Foreign Trade

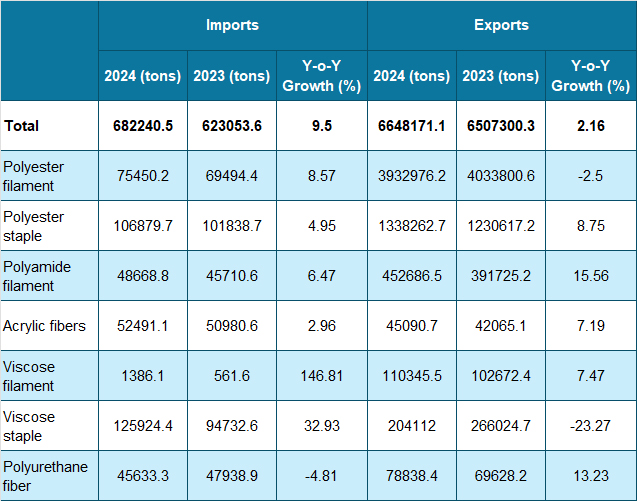

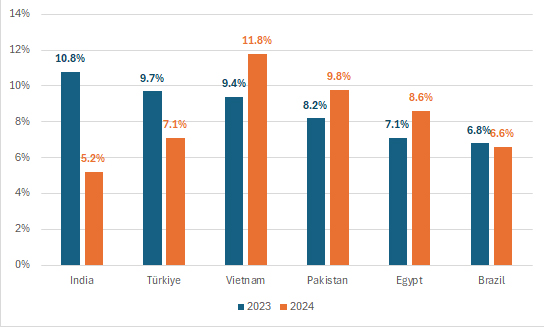

According to China Customs data, the exports of major chemical fiber products totaled 6.65 million tons in 2024, growing by 2.16% year over year (Table 2). By destination, India’s export volume experienced a significant reduction. In October 2023, India implemented BIS certification on polyester filament. Therefore, Chinese enterprises were urged to export, resulting in a sharp increase in polyester filament exports in 2023. While the exports last year did not continue the previous year's high-growth trend, the annual export volume decreased by 2.50% year-on-year. But when excluding India, exports of polyester filament to other countries and regions are actually growing. In addition, the chemical fiber export market share changes significantly (Figure 1). India and Türkiye’s share fell by 5.6 and 2.6 percentage points, respectively, while Vietnam, Pakistan, and Egypt’s share increased significantly.

Table 2: Foreign Trade of China’s Chemical Fiber Products in 2024

Figure 1: Changes in Market Share for China’s Major Chemical Fiber Export Destinations

IV. Revenue & Benefits

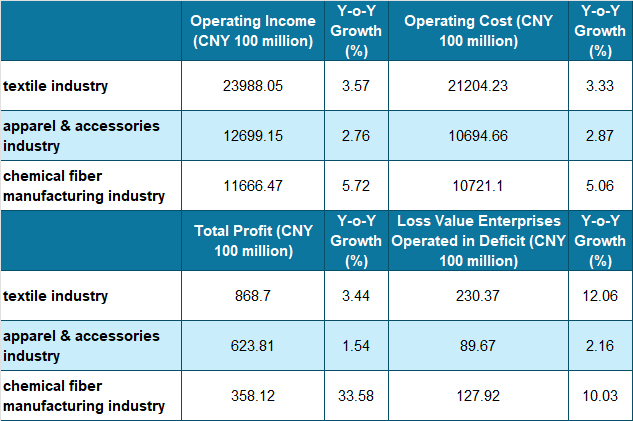

According to the National Bureau of Statistics data, the operating revenue of China’s chemical fiber industry totaled 1.16 trillion yuan last year, an increase of 5.72% year over year. Their total profit reached 35.8 billion yuan, surging by 33.58% year over year. The base effect gradually narrowed the profit growth. The operating income margin was 3.07%, which is still at a relatively low level in recent years, but is on an upward trend month-on-month. The chemical fiber industry contributes about 18.5% of the textile industry’s profit, 3.6 percentage points higher than in 2023.

By sub-industry, the profits of polyester fiber, polyamide fiber, and cellulose fiber significantly improved in 2024, contributing 48%, 18%, and 23% to the profits of the chemical fiber industry, respectively. Specifically, the polyester sector faced some pressure on its profits in the first half of 2024, but it improved in the second half. The profit performance of the polyamide fiber industry was more stable: strong demand in the outdoor and sportswear sectors drove growth in polyamide consumption. The overall decline in profit for the spandex industry was more pronounced due to falling raw material prices and supply pressures. Demand did not meet expectations, resulting in a relatively high inventory level, and product prices are showing a downward trend.

Table 3: Economic Benefit of China’s Chemical Fiber and Related Industries in 2024

Source: National Bureau of Statistics

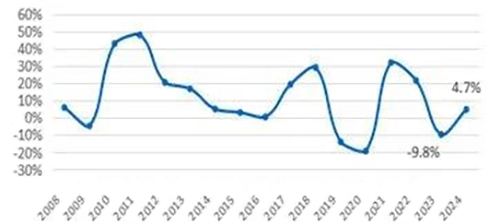

V. Fixed-assets Investment

According to the National Bureau of Statistics, fixed-asset investment in the chemical fiber industry increased by 4.7% year-on-year in 2024, compared to -9.8% in 2023. This growth rate rebounded due to the low base effect. Regarding new production capacity, the new capacity for polyester fibers reached 1.96 million tons per year. Additionally, companies are increasingly focusing on enhancing the original production capacity through high-end, intelligent, environmentally friendly upgrades and transformations.

Figure 2: Fixed-Assets Investment Growth of the Chemical Fiber Industry from 2008 to 2024

Source: National Bureau of Statistics

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay