2024/12/24

I.Production

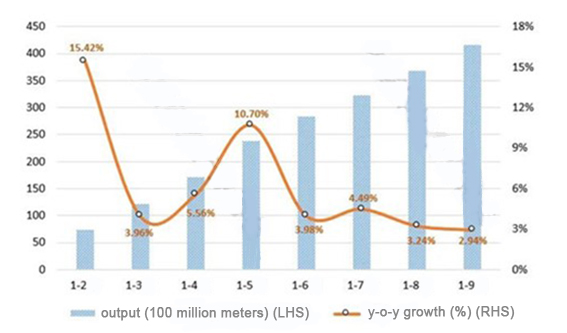

The data released by the National Bureau of Statistics revealed that the output of printed and dyed fabrics above the designated size in the printing and dyeing industry totaled 41.62 billion meters in the first three quarters, up by 2.94% year-on-year, 1.04 percentage points lower than the growth rate of the first half. In the third quarter, the production situation of China’s printing and dyeing industry turned weak. The monthly output of printed and dyed fabrics was lower than 5 billion meters; compared with the second quarter, the average monthly production fell more than 10%. From the perspective of monthly performance, the Chinese printing and dyeing industry went into the traditional off-season in July. Enterprise production orders have been reduced, and the start-up rate has dropped, but the monthly output has slightly increased year-on-year. In September, enterprise production improved due to increased fabric orders in autumn and winter. The output of printed and dyed fabrics reached 4.89 billion meters in September, seeing a month-on-month growth of 3.64%.

Figure 1: Printed and Dyed Fabrics Output of Enterprises Above Designated Size in China in Q1-Q3, 2024

Source: National Bureau of Statistics

II. Exports

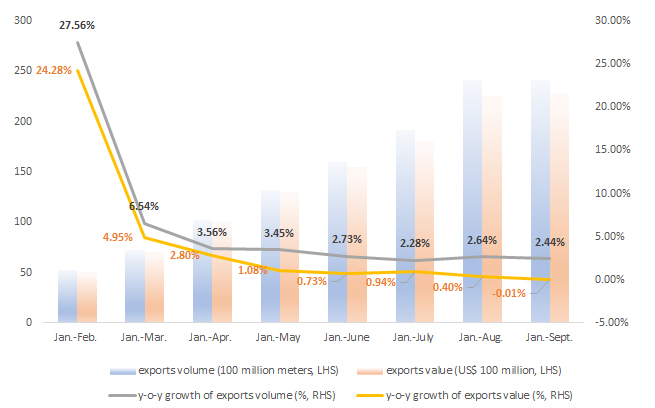

According to the statistics released by China General Customs, the export volume of eight major categories of printed and dyed products, i.e., dyed cotton fabric, printed cotton fabric, dyed cotton-blended fabric, printed cotton-blended fabric, synthetic filament fabric, polyester staple fabric, printed and dyed T/C fabric, man-made staple fabric, totaled 24.19 billion meters in the first three quarters of 2024, up by 2.44% year-on-year. The export value reached US$ 22.72 billion, with a slight year-on-year decrease of 0.01%. The average export unit price was US$ 0.94/meter, declining by 2.39% year-on-year.

In the first three quarters, China’s major printed and dyed products showed increased export volume and decreased export price. The average export unit price hit the new lowest in the same period of nearly a decade, and the decline rate was expanding, which applied greater competitive pressures on the industry’s exports.

Weak external demand is an important reason for the industry’s export pressure. Although the inflation rate of major developed countries showed a downward trend this year, the global trade dynamics were still weak, and the manufacturing PMI index remained in the contraction zone. Overall, demand for China’s textiles and apparel in the international market showed a weak recovery. From January to September, China’s textile and apparel exports totaled US$ 222.41 billion, seeing a year-on-year increase of 0.5%, 1.0 percentage points lower than the first half of this year. Meanwhile, the trend of industrial transfer promoted the printing and dyeing production capacity increase in Southeast Asia, South Asia and other regions, which formed direct competition to China’s printing and dyeing products exports, further increasing the pressure on the industry’s foreign trade.

Figure 2: The Export Growth Rate of Eight Major Categories of Printed and Dyed Products in China in Q1-Q3, 2024

ASEAN is China’s most important export market for printed and dyed products. In the first three quarters, the export volume of eight major categories of printed and dyed products to the ASEAN amounted to 5.72 billion meters, surging by 8.77% year-on-year, 6.33 percentage points higher than the growth rate of the total export amount. The average export unit price was US$1.20/meter, declining by 0.02% year-on-year. Driven by the export growth to ASEAN, the exports of the RCEP member countries, of which ASEAN countries are an important component, performed well. From January to September, the export volume of eight major categories of printed and dyed products to the RCEP member countries reached 6.1 billion meters, up by 7.94% year-on-year, with US$ 7.2 billion worth of export amount, ballooning by 7.65% year-on-year.

From the perspective of the main export destinations, the exports of the top ten destinations of China’s eight major categories of printed and dyed products reached 10.25 billion meters, accounting for 42.39% of the total. Among them, the exports to Vietnam, Bangladesh, and Brazil achieved double-digit growth, and India and the Philippines also witnessed a slight increase. Vietnam and Bangladesh are important global textile and apparel export destinations. Supported by preferential tariff policy support from developed economies and the rapid recovery of the local textile and garment industry, Vietnam and Bangladesh’s textile and garment trade improved significantly, promoting high demand for China’s printed and dyed products. As a populous country, Brazil also boasts unique advantages in the North American re-export trade, resulting in gradually increased demand for China’s printed and dyed products.

In the first three quarters, as for the top ten destinations, only Vietnam and Myanmar’s unit price of exports increased slightly; the rest of the countries showed a downward trend, of which the Philippines and Pakistan saw a larger decline. Insufficient market demand superimposed on the gradual release of local printing and dyeing capacity, China’s printing and dyeing industry exports faced further pressure. Boosting export volume with low prices has become a common strategy for enterprises to stabilize development.

Table: Performance of Top Ten Destinations of China’s Eight Major Categories of Printed and Dyed Products in Q1-Q3, 2024

Source: China Customs

III. Operation quality and efficiency

According to the National Bureau of Statistics data, the share of three overheads in turnover was 6.89% in the first three quarters of 2024, down 0.08 percentage points year-on-year. The turnover rate of finished products was 13.69 times/year, down 1.61% year-on-year; the turnover of accounts receivable was 8.06 times/year, seeing a year-on-year decline of 0.85%; and the total asset turnover was 0.99 times/year, increasing by 4.09% year-on-year. In the first three quarters, the main operational quality indicators of China’s printing and dyeing industry recovered from that of the first half, but the overall performance was still weak. Affected by the lack of demand, the market competition intensified, the sales cost increased, and the turnover rate of finished goods decreased. From January to September, the sales costs of printing and dyeing enterprises above the designated size surged by 11.49% year-on-year, 3.38 percentage points higher than the operating income growth rate.

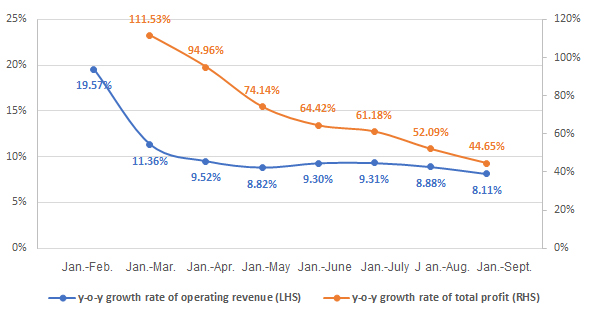

The National Bureau of Statistics data showed that the operating income of China’s printing and dyeing enterprises above the designated size totaled 235.38 billion yuan from January to September, seeing a year-on-year increase of 8.11%. Their profits totaled 10.56 billion yuan, ballooning by 44.65% year-on-year. Its ratio of profits to cost was 4.83%, up by 1.26 percentage points year-on-year. The sales profit margin was 4.49%, 1.14 percentage points higher than the same period of last year. 34.26% of printing and dyeing enterprises operated in deficit with 2.59 billion yuan of loss value, which decreased by 9.80% year-on-year.

In the first three quarters, the operating income and total profits of China’s printing and dyeing industry increased faster. Total profits hit the highest level in recent years, increasing 8.18% over the same period in 2019. It should be noted that the loss still expanded in the first three quarters, indicating that although the overall profitability marked improvement, the market competitiveness of different enterprises there showed obvious differences.

Figure 3: Main Economic Indicators of the Printing and Dyeing Enterprises Above the Designated Size in Q1-Q3, 2024

Source: National Bureau of Statistics

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay