2024/9/24

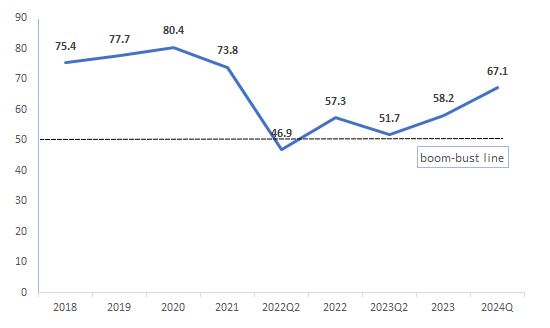

In the first half of 2024, the complexity and severity of the external environment uncertainty rose significantly; the domestic structural adjustment continued to deepen, and other new challenges emerged. However, the recovered external demand, accelerated development of new quality productivity, and other factors also formed new support. Market demand in China’s technical textile industry rebounded in general; the impact of large fluctuations in demand brought about by the COVID-19 pandemic has basically receded. The industry’s industrial-added value growth rate has been rising since the beginning of 2023. According to the China Nonwovens & Industrial Textile Association (CNITA) research, the prosperity index of China’s technical textile industry was 67.1 in the first half of 2024, seeing a significant rebound compared with the same period in 2023 (51.7) (Figure 1).

Figure 1: Prosperity Index of China’s Technical Textile Industry

Source: China Nonwovens & Industrial Textile Association (CNITA)

I.Market Demand and Production

According to the CNITA research on member enterprises, the market demand for the technical textile industry recovered significantly in the first half of 2024, with domestic and international order indexes reaching 57.5 and 69.4, respectively, compared with the same period of 2023 (37.8 and 46.1), which rebounded significantly. In terms of sub-fields, the domestic market for medical and hygiene textiles, specialty textiles, and twine, rope, and cable continued to recover, and there were obvious signs of a rebound in international market demand for filtration and separation textiles, nonwovens, and medical and hygiene textiles.

The recovery of market demand drove the steady growth of production. According to the Association’s research, the capacity utilization rate of technical textile enterprises was about 75% in the first half of 2024, among which the capacity utilization rate of spunbond and spunlace nonwovens enterprises was around 70%, which was better than the level of the same period in 2023.

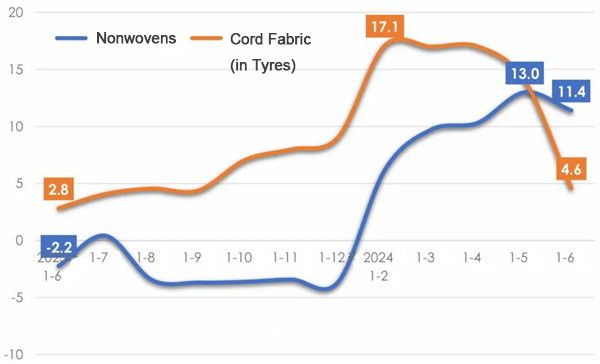

According to data from the National Bureau of Statistics, the output of nonwoven enterprises above designated size increased by 11.4% year-on-year in the first half. And the output of cord fabric (in tyres) saw year-on-year growth of 4.6%, with a slight decrease. (Figure 2)

Figure 2: Output Growth Rate of Nonwoven and Cord Fabric (in Tyres) Enterprises Above Designated Size

Source: National Bureau of Statistics

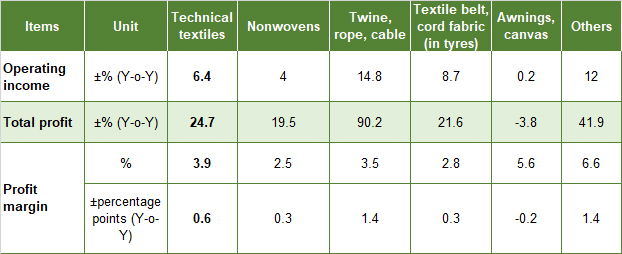

II.Economic Benefit

Affected by the high base brought by the epidemic prevention materials, the operating income and total profits of China’s technical textile industry have decreased from 2022 to 2023. In the first half of 2024, supported by market demand, the operating income and total profits surged by 6.4% and 24.7% year-on-year, respectively, stepping into the growth channel again. According to the CNITA research, enterprises’ orders in the first half of 2024 were generally better than those in 2023. Still, fierce competition in the low-end and middle-end markets put greater downward pressure on product prices. Some enterprises focusing on niche and high-end markets said that functionalized and differentiated products could still maintain a certain degree of profitability.

Table 1: Growth Rate of Major Economic Indicators of China’s Technical Textile Industry in H1, 2024

(Above Designated Size)

Source: National Bureau of Statistics, China Nonwovens & Industrial Textile Association (CNITA)

III.Foreign Trade

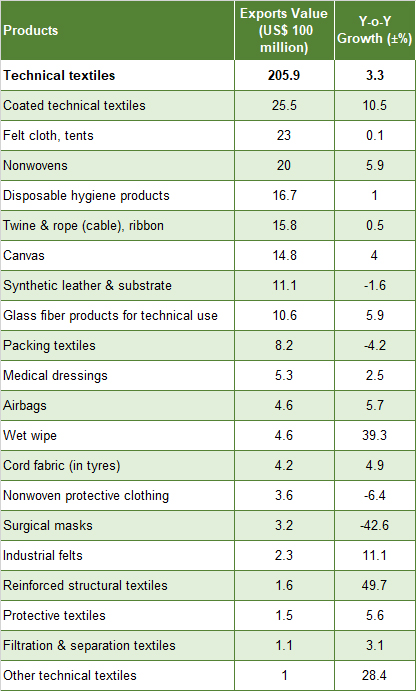

According to China Customs, China’s technical textile industry exported US$ 20.59 billion worth of products from January to June 2024, seeing a year-on-year growth of 3.3%. The industry’s import value (customs 8-digit HS code statistics) amounted to US$ 24.6 billion, down by 5.2% year-on-year.

In the first half of 2024, the key products of China’s technical textile industry (Chapters 56 and 59) have maintained a high growth rate of exports to major markets. For example, the exports to Vietnam and the United States ballooned by 24.4% and 11.8%, respectively, and exports to Cambodia surged by nearly 35%. However, exports to India and Russia have declined by more than 10%. The market share of developing countries in China’s technical textile export is increasing.

From the perspective of major export products, the export value of key export products such as coated technical textiles, felt cloth, tents, nonwovens, disposable hygiene products, twine & rope (cable), ribbon, canvas, glass fiber products for technical use all maintained a certain degree of growth in the first half of 2024; the exports of wet wipe, and reinforced structural textiles maintained a higher rate of growth. Overseas demand for disposable hygiene products such as diapers and sanitary napkins has contracted. Although their exports maintained growth, their growth rate has been slumped by 20 percentage points compared with the same period in 2023.

Regarding export prices, except for coated technical textiles, airbags, filtration & separation textiles, and other technical textiles saw an increase in prices, the prices of the rest of the products have declined to vary degrees.

Table 2: The Exports of Main Products in China’s Technical Textile Industry in H1, 2024

Source: China Customs, China Nonwovens & Industrial Textile Association (CNITA)

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay