2026/2/28

In 2025, the international landscape continued to evolve amid heightened turbulence, great-power competition intensified, and geopolitical conflicts persisted. Against this backdrop, global economic recovery remained sluggish, national growth trajectories diverged, overall market demand weakened, and trade protectionism accelerated the restructuring of the world’s economic and trade order, significantly increasing uncertainty in international markets.

Faced with rapidly shifting external conditions and short-term pains from domestic economic transformation, China’s dyeing and finishing industry adhered to the principle of “stability while seeking progress, and progress reinforcing stability.” The sector responded proactively to risks and challenges, maintaining generally stable operations throughout the year. Dyed fabrics output continued to grow, and export volumes of key products reached a new record high. However, the industry faced substantial pressure on both market performance and profitability, with major economic indicators showing clear declines. The foundation for sustained, high-quality development thus requires further consolidation.

I. Production Remained Stable with Modest Growth

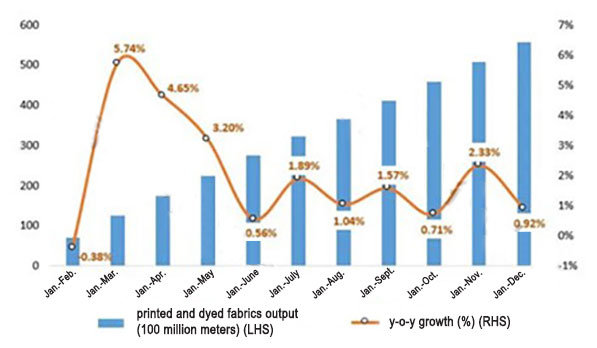

According to data from the National Bureau of Statistics (NBS), from January to December 2025, dyed fabric output from enterprises above the designated size in the dyeing and finishing industry increased by 0.92% year-on-year, though this represented a 0.65-percentage-point slowdown compared to the first three quarters (see Figure 1).

Figure 1: Printed and Dyed Fabrics Output of Enterprises Above Designated Size in China in 2025

In the fourth quarter, monthly production volumes rose month-on-month, but all recorded year-on-year declines, with December alone down 6.69%. Since September 2025, domestic demand for textiles and apparel has shown insufficient momentum, diminishing the drive to dyeing production.

Retail sales of apparel, footwear, and knitwear from enterprises above the designated size grew by 3.2% for the whole year, but December’s year-on-year growth slowed sharply to just 0.6%, down 5.7 percentage points from the October peak. Online retail sales of wearing goods rose by 1.9% year-on-year, a 0.9-percentage-point deceleration from the first nine months. Overall, the industry’s production trajectory in 2025 followed a pattern of “pressure at the start of the first quarter, slowing growth in the second quarter, and low-speed stabilization in the third and fourth quarters”, heavily influenced by weak domestic and overseas demand.

II. Exports Faced Pressure Yet Demonstrated Strong Resilience

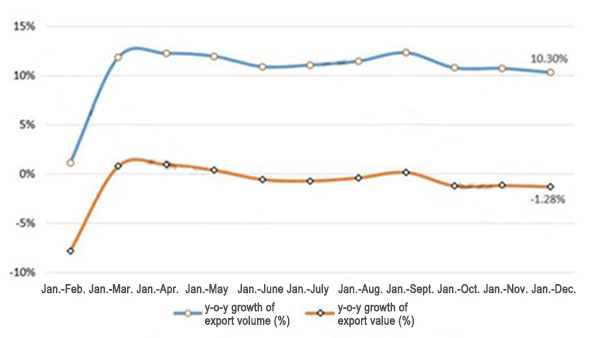

According to data from China Customs, from January to December 2025, the export volume of eight major categories of printed and dyed products, i.e., dyed cotton fabric, printed cotton fabric, dyed cotton-blended fabric, printed cotton-blended fabric, synthetic filament fabric, polyester staple fabric, printed and dyed T/C fabric, man-made staple fabric, reached 36.99 billion meters, up 10.30% year-on-year (a 2.00-percentage-point slowdown from Q1–Q3; see Figure 2). Their export value totaled US$30.89 billion, down 1.28% (a 1.46-percentage-point worsening). Average export price fell to US$0.84 per meter, a 10.50% decline (though the rate of decline narrowed by 0.29 percentage points). While the exports of the fourth quarter moderated relatively due to a high base from the prior year’s “rush-to-export” behavior, the overall export scale remained relatively stable.

Figure 2: The Export Growth Rate of Eight Major Categories of Printed and Dyed Products in China in 2025

Despite global growth slowdowns, weak demand, and U.S. tariff policies that pressured textile exports, China’s printing and dyeing industry retained strong international competitiveness, underpinning global textile supply chains. Notably, export volumes hit an all-time high in 2025, with cumulative growth of 59.97% since the start of the 14th Five-Year Plan period (2021-2025). However, export value growth lagged far behind volume growth, as average unit prices fell to their lowest level since 2007. Tariff disruptions and soft demand intensified price-based competition.

ASEAN, a key export destination of China’s printing and dyeing industry, saw that the export volume was 8.32 billion meters (+5.16%, 5.14 ppt below the overall growth rate); export value reached US$8.83 billion (–5.92%, 4.64 ppt worse than the average); average price was US$1.06/meter (–10.53%). However, U.S. “reciprocal tariffs” and higher transshipment duties led to a notable slowdown in ASEAN-bound exports. ASEAN’s share of China’s total exports in terms of the printing and dyeing industry dropped from 23.58% to 22.48% (–1.10 ppt). Exports to RCEP members also underperformed the overall average.

Conversely, as shown in the table, exports to the top 10 destination countries surged by 15.85% to 16.71 billion meters, accounting for 45.19% of total exports, a 2.03-percentage-point increase in concentration. Nigeria alone contributed 54.34% of the incremental volume, with exports soaring 51.48% to 3.66 billion meters. Strong growth was also seen in Pakistan, India, Myanmar, and Cambodia, while traditional markets like Vietnam and Bangladesh lagged significantly, reflecting strategic market diversification in response to U.S. trade pressures. China’s printing and dyeing industry is actively adjusting its market structure and accelerating the expansion of emerging market development opportunities, effectively responding to external shocks through industrial resilience. Average export prices to all top 10 countries declined, with Vietnam seeing the steepest drop at –15.06%.

Table: Performance of Top Ten Destinations of China’s Eight Major Categories of Printed and Dyed Products in 2025

In 2025, the SG&A ratio in the printing and dyeing industry increased, leading to rising cost pressures, squeezed profit margins, and operational difficulties for enterprises. Key operational efficiency indicators showed a significant downward trend, with overall industry operational efficiency remaining low, extended capital recovery cycles, and reduced efficiency in production-sales coordination. Based on data released by the National Bureau of Statistics, in 2025, the SG&A ratio rose to 7.38% (+0.49 ppt), with that of cotton dyeing at 7.27% and synthetic fiber finishing at 7.72%; finished goods turnover slowed to 12.49 times/year (–9.76%); accounts receivable turnover fell to 6.90 times/year (–10.65%); total asset turnover dropped to 0.88 times/year (–11.87%).

III. Operational Efficiency Under Significant Pressure; Enterprise Difficulties Mount

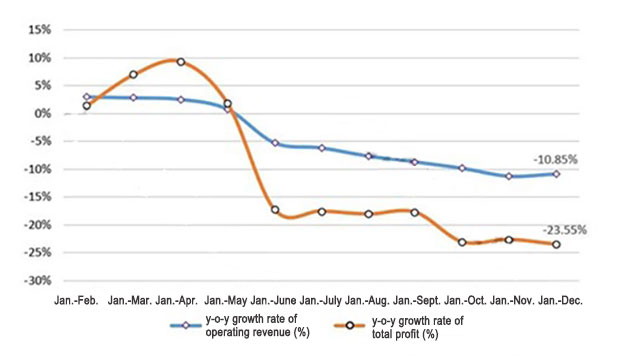

In 2025, affected by weak terminal demand and intensified export competition, production and operational pressures on printing and dyeing enterprises rose significantly, while operational quality and efficiency continued to decline. According to data from the National Bureau of Statistics, from January to December 2025, revenue from large-scale enterprises fell by 10.85% year-on-year (decline deepened by 2.14 ppt compared to that of the first nine months); total profits plunged by 23.55% (worsened by 5.79 ppt); The ratio of profit to total cost stood at 5.03% (–0.84 ppt); operating profit margin was 4.64% (–0.77 ppt). Among 1,869 large-scale enterprises, 616 reported losses (loss ratio: 32.96%, up 3.03 ppt), with total losses reaching 3.65 billion yuan (+19.96%). Compared to the broader textile industry, the dyeing sector fared worse: its revenue and profit declines were 2.62 and 7.43 percentage points deeper, respectively, and its loss ratio was 10.32 ppt higher.

Figure 3: Main Economic Indicators of the Printing and Dyeing Enterprises Above the Designated Size in 2025

IV. Outlook for 2026

Looking ahead to 2026, the global economy remains vulnerable to downside risks. Tariff volatility, geopolitical tensions, and fiscal constraints could trap the world in a state of “low growth and weak resilience.” Global trade and supply chains are rapidly reconfiguring, shifting from “efficiency-first” to “security-first” models, with growing emphasis on diversification and “friend-shoring.” Rising trade barriers will further dampen global trade, while weak consumer demand in key markets—exacerbated by protectionism—will prolong demand-side weakness. Meanwhile, U.S.-led decoupling efforts and escalating tariffs are prompting leading Chinese dyeing firms to accelerate the deployment of overseas capacity, potentially affecting the stability and security of China’s domestic textile supply chain.

Domestically, CPI remains subdued, and PPI stays in negative territory, reflecting persistent oversupply relative to weak demand. Consumer confidence and effective demand are unlikely to rebound sharply in the near term. Nevertheless, China’s macroeconomy continues to demonstrate strong fundamentals, abundant advantages, robust resilience, and vast potential. The country’s massive and upgrading domestic market serves as the “ballast stone” for industry stability, while its integrated industrial chain and innovation leadership form the core pillars of competitiveness and high-quality development.

The Central Economic Work Conference has prioritized expanding domestic demand as the top task for 2026. As existing and new supportive policies take effect, multiplier effects and structural dividends are expected to unlock significant new consumption potential, fostering sustained and healthy industry growth.

Overall, opportunities outweigh challenges for the dyeing and finishing industry in 2026. The sector is expected to maintain stable production and export volumes, with operational efficiency likely to stabilize and recover from the low base of 2025. The industry’s transformation toward high-end, intelligent, green, and integrated development will become increasingly evident.

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay