2025/6/20

In the first quarter of 2025, China’s economy ushered in a good start, with GDP (constant prices) growing by 5.4% year-on-year in the current quarter, exceeding the expected growth target of “around 5.0%.” In this context, the chemical fiber industry continued its growth trend, maintaining a relatively high starting load and showing a year-on-year increase in production. Prices have exhibited a downward trend, resulting in a year-on-year decline in operating income; however, total profits have continued to grow. Export performance has been notably strong, with the front-loading export effect contributing to an increase in the export growth rate.

I. Production & Inventory

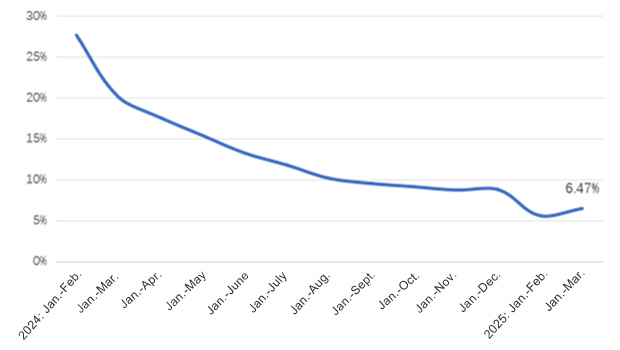

In the first quarter, the overall production of the chemical fiber industry was strong, though the starting loads for subsectors varied. Among them, the starting load for direct spinning polyester filament increased each month, averaging 85% in January, rising to 89% in February, and reaching 94% in March. The nylon civil filament maintained an average starting load of 82% for the first quarter, which was essentially the same as in 2024. In contrast, the spandex average starting load was 79%, marking a decline of 2.8 percentage points from the same period in 2024. Since April, the trade conflict between China and the U.S. has intensified, deepening the negative external impact. Influenced by the macroeconomic environment, the chemical fiber industry’s starting load has decreased. According to the National Bureau of Statistics, the chemical fiber output totaled 20.63 million tons in the first quarter of 2025, seeing a year-on-year growth of 6.47% (Figure 1).

Figure 1: The Growth Rate of Chemical Fibers Output from the Beginning of 2024

Source: National Bureau of Statistics, China Chemical Fibers Association (CCFA)

II. Market & Price

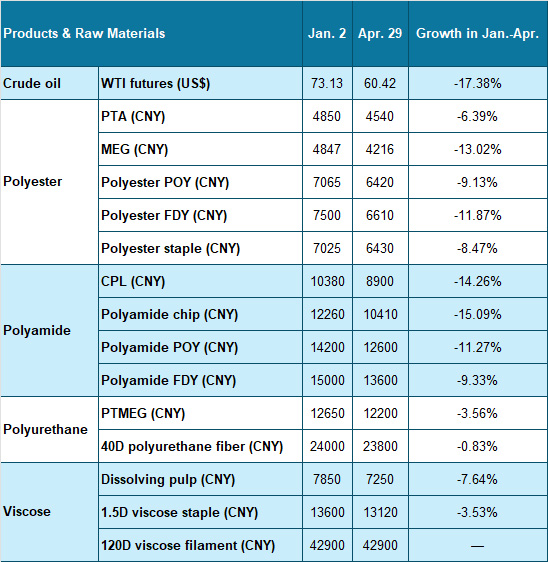

Since the beginning of 2025, crude oil prices have gradually declined due to a combination of supply-demand imbalances, geopolitical conflicts, a weak global economic recovery, changes in tariff policies, and increasing risk aversion. The prices of major products and raw materials in the chemical fiber sector have also trended downward. Among other sub-industries, the polyamide industry chain has seen a more significant decline (Table 1).

Table 1: Price Change of Main Chemical Fibers and Raw Materials Since the Beginning of 2025

III. Foreign Trade

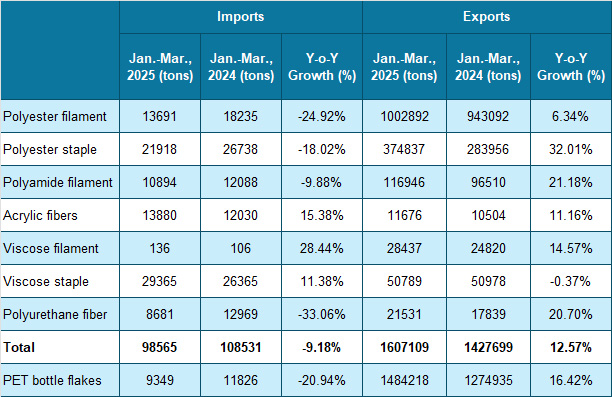

According to China Customs, from January to March, the export of chemical fiber products totaled 1.61 million tons, reflecting a year-on-year increase of 12.57%. Among them, polyester staple exports soared by 32.01% year-on-year, with exports to Vietnam, Pakistan, and Brazil ranking as the top three, showing surges of 16.52%, 84.55%, and 73.08% year-on-year, respectively.

Table 2: Foreign Trade of Chemical Fiber Products in Q1, 2025

Source: Based on data from China Customs

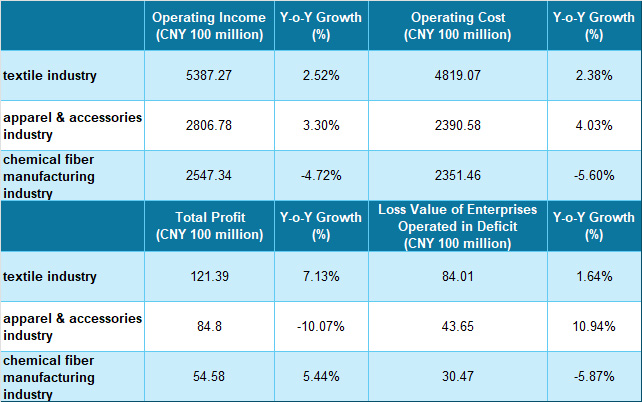

IV. Revenue & Benefits

Crude oil prices declined in the first quarter, and the drop in raw material costs led midstream and downstream companies to experience improved profit margins. Data from the National Bureau of Statistics show that the total profit of the chemical fiber industry grew by 5.44% in the first quarter; however, due to the effect of falling chemical fiber prices, operating income decreased by 4.72% year-on-year (Table 3). The profit margin for the main business is 2.14%; the total loss for companies operating at a deficit reached 3.05 billion yuan, marking a year-on-year decline of 5.87%.

Table 3: Economic Benefit of Chemical Fiber and Related Industries in Q1, 2025

Source: National Bureau of Statistics

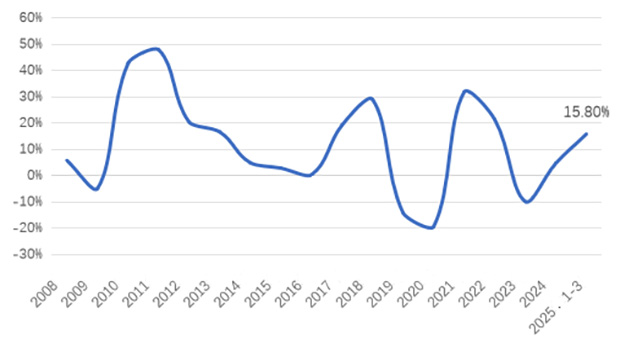

V. Investment

Data from the National Bureau of Statistics indicate that fixed-asset investment in the chemical fiber industry rose by 15.8% year-on-year in the first quarter. The ongoing renewal of large-scale equipment remains the primary driving force, enhancing investment growth in the industry.

Figure 2: Fixed-Assets Investment Growth of the Chemical Fiber Industry from 2008 to Q1, 2025

Source: National Bureau of Statistics

VI. Forecast

Regarding raw materials in the chemical fiber industry, several institutions predict that the crude oil market will exhibit a pattern of oscillation with a downward bias in 2025, with benchmark prices shifting downward compared to 2024. Crude oil prices are expected to weaken, and chemical fiber prices will likely remain in a lower-range oscillation. However, the decline in raw material costs is also anticipated to expand the industry’s profit margins.

Regarding the supply side, by 2025, the industry will still face pressure from new production capacity, and the “strong supply and weak demand” pattern is expected to persist. The supply-demand gap still needs to narrow. Companies must enhance self-discipline in the industry to ensure smooth operations and healthy development. On the demand side, key categories of supported goods grew significantly, driven by the consumer goods trade-in policy. However, service-oriented retail weakened, indicating that residents’ consumption expectations remain cautious, and their consumption capacity still needs to be restored. With the combined effect of incremental and stock policies, the growth rate of service and commodity consumption is expected to improve. Regarding foreign sales, the U.S.-China talks in Geneva reached a critical consensus and made substantial progress, suggesting that textile and garment exports are expected to see short-term growth.

Looking ahead to the whole year, the policy release is worth anticipating, but the chemical fiber industry still faces operational pressures. From the perspective of data indicators, although the chemical fiber industry is displaying a recovery growth trend in 2024, the expected growth rate of the indicators in 2025 is likely to remain relatively low.

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay