2025/3/20

I. Production

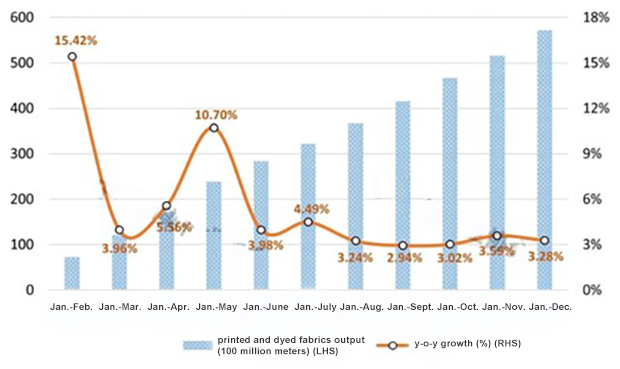

According to the National Bureau of Statistics, the output of dyed fabrics by enterprises above designated size in the printing and dyeing industry increased by 3.28% year-on-year in 2024, and the growth rate increased by 0.34 percentage points compared with that of the previous three quarters. In the fourth quarter, the production of the printing and dyeing industry gradually improved. The output of printed and dyed fabric picked up month by month, and that of each month remained above 5 billion meters. Among these, the output of printed and dyed fabric reached 5.93 billion meters in December of 2024, up by 6.01% year-on-year, which was the highest level since March. For the whole year, the total retail sales of clothing, foot and head wear, and knitwear above designated size increased by 0.3% year-on-year, and the online retail sales of wearing goods grew by 1.5% year-on-year, with the growth rate dropping by 12.6 and 9.3 percentage points compared with that of the previous year respectively. Affected by the slow recovery of textile and apparel consumption, the output of China’s printed and dyed fabric showed a decline in the first half and gradual stabilization in the second half.

Figure 1: Printed and Dyed Fabrics Output of Enterprises Above Designated Size in China in 2024

II. Exports

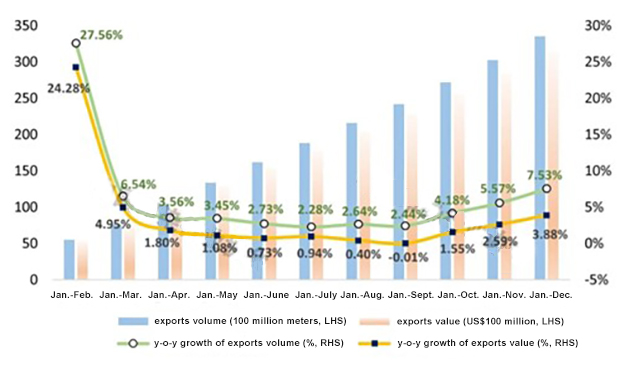

According to the statistics released by China General Customs, the export volume of eight major categories of printed and dyed products, i.e., dyed cotton fabric, printed cotton fabric, dyed cotton-blended fabric, printed cotton-blended fabric, synthetic filament fabric, polyester staple fabric, printed and dyed T/C fabric, man-made staple fabric, totaled 33.53 billion meters in 2024, up by 7.53% year-on-year, 5.09 percentage points higher than that of the first three quarters. The export value reached US$31.29 billion, with a year-on-year growth of 3.88%. The average export unit price was US$0.93/meter, declining by 3.39% year-on-year. In the fourth quarter, with the arrival of Thanksgiving, Christmas, and other holidays aboard, the demand for replenishing inventory of textiles and apparel gradually released. Coupled with that, the U.S. government’s potential tariffs on China’s exports led to the adjustment of China’s textile and apparel enterprises’ foreign trade plan. The short-term export boost further promotes the export growth rate of printed and dyed products.

Throughout the year, despite the weak demand in the international market and the high risk of the global trade environment, China’s printing and dyeing industry, by virtue of industrial chain advantages, scale advantages, technological advantages, talent advantages and product advantages, etc., still has significant competitiveness in the international market. The export scale of China’s eight major categories of printed and dyed products hit a new record after achieving more than 30 billion meters in 2023. The industry’s exports showed a stronger resilience. However, it is worth noting that the average unit price of the major printed and dyed products exported still maintained the downturn since 2023 and has fallen to the lowest level in the past 15 years in 2024, reflecting the impact of the global economy, the slow recovery of the international market demand, and the mismatch between supply and demand leading to further intensification of the industry export competition.

Figure 2: The Export Growth Rate of Eight Major Categories of Printed and Dyed Products in China in 2024

In 2024, the exports of China’s printing and dyeing industry to ASEAN and RCEP member countries achieved faster growth in scale; the growth rate was higher than the overall export level but also presented an increase in volume and a decline in price. The export volume of eight major categories of printed and dyed products to the ASEAN amounted to 7.9 billion meters in 2024, surging by 12.14% year-on-year, 4.61 percentage points higher than the growth rate of the total export amount. Its exports account for 23.58% of the total. The average export unit price was US$1.19/meter, declining by 2.75% year-on-year. During the same period, the export volume of eight major categories of printed and dyed products to the RCEP member countries reached 8.43 billion meters, up by 11.35% year-on-year. The average export unit price was US$1.17/meter, declining by 2.79% year-on-year.

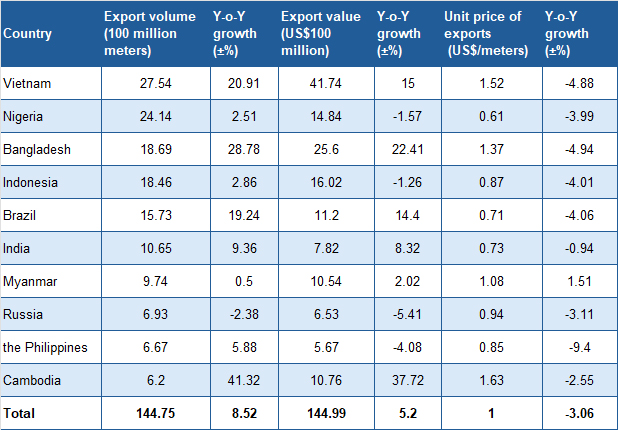

From the perspective of the main export destinations, the exports of the top ten destinations of China’s eight major categories of printed and dyed products reached 14.47 billion meters, accounting for 43.16% of the total. Among them, only the exports to Russia fell slightly by 2.38%; exports to the rest of the countries have varying degrees of growth, of which the exports to Cambodia surged by 41.32% year-on-year. Cambodia replaced Pakistan for the first time in entering the top ten export destinations. The exports to Vietnam and Bangladesh ballooned by more than 20%. These two countries are the world’s important textile and apparel exporters, showing an increased demand for China’s printed and dyed fabrics. The export growth rate to Nigeria, Indonesia, Myanmar, and the Philippines was not as fast as the overall level, and the exports to Pakistan fell sharply by 27.71% year-on-year. And Pakistan’s export ranking slipped to 11th place. Myanmar is the only one of the top ten countries to realize the increase in both volume and price.

Table: Performance of Top Ten Destinations of China’s Eight Major Categories of Printed and Dyed Products in 2024

III. Operation quality and efficiency

In 2024, most of the printing and dyeing industry’s operating quality indicators show a recovered tendency. Enterprise cost control has achieved results; production and marketing convergence is smoother; asset utilization efficiency is high; however, low capital turnover efficiency, an extended accounts recovery cycle, and other issues affect the stability of business operations, production, and investment to some extent. According to the National Bureau of Statistics data, the share of three overheads in turnover was 6.90% in 2024, down 0.05 percentage points year-on-year. The turnover rate of finished products was 13.92 times/year, up 0.55% year-on-year; the turnover of accounts receivable was 7.70 times/year, seeing a year-on-year decline of 3.89%; and the total asset turnover was 0.99 times/year, increasing by 2.47% year-on-year.

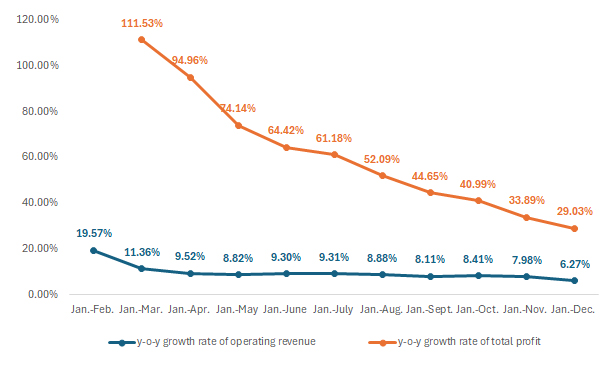

In terms of operating efficiency, since 2024, the growth rate of operating income and total profit of the printing and dyeing industry has generally shown a month-by-month slowdown. However, the whole year showed faster growth, and operating income and total profit hit the highest since 2018. The National Bureau of Statistics data showed that the operating income of China’s printing and dyeing enterprises above the designated size saw a year-on-year increase of 6.27%. Their profits ballooned by 29.03% year-on-year. The sales profit margin was 5.51%, 0.97 percentage points higher than the same period of the previous year. 29.93% of printing and dyeing enterprises operated in deficit with 2.88 billion yuan of loss value, which decreased by 14.91% year-on-year.

In 2024, the operating efficiency of China’s printing and dyeing industry improved significantly as a whole. Its annual operating income and total profit growth rate were 2.31 and 21.49 percentage points higher than that of the textile industry; the sales profit margin was 1.60 percentage points higher than the textile industry, but the industry loss was still 9.10 percentage points higher than the textile industry, reflecting the further profitability differentiation of current printing and dyeing enterprises. The profitability level of flagship printing and dyeing enterprises continued to improve, while some small and medium-sized enterprises were still facing greater profitability pressure.

Figure 3: Main Economic Indicators of the Printing and Dyeing Enterprises Above the Designated Size in 2024

Looking ahead to 2025, the global economic situation remains complex and volatile, with many uncertainties leading to a test of the sustainability and balance of the recovery process. The International Monetary Fund (IMF) expects the global economy to remain resilient in 2025. The growth rate is expected to be maintained at 3.2%. Still, the increasing trade tensions, the rising risk of trade protectionism, and the possible escalation of geopolitical conflicts will have far-reaching impacts on the global economy. Meanwhile, Europe, the United States, and other Western countries implemented “nearshoring” or “friend-shoring”; the global supply chain pattern will accelerate the adjustment. China’s printing and dyeing enterprises may face a series of problems, such as shrinking orders, loss of customers, and rising costs. In addition, the United States imposed tariffs on China’s textile products, which will further weaken the competitiveness of China’s textile and apparel exports. As for the domestic market, the lack of consumption willingness, delayed consumption structure upgrading, and other issues constrain the economy’s steady growth. The domestic demand market still needs to be consolidated to restore the foundation.

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay