2025/2/26

In 2024, in the face of the complex and severe development environment, China’s apparel industry fully stimulated its development potential. The domestic market performed stable under pressure; exports showed resilience; production, investment, efficiency, and other major operating indicators improved significantly; and the industry’s economic operation was generally stable. Looking forward to 2025, China’s apparel industry will adhere to the new positioning of the “sci-tech, fashion, green, healthy” industry, continue to optimize the industrial structure and accelerate the cultivation of new productivity and high-quality development.

I. Economic Operation of the Apparel Industry in 2024

01. Production

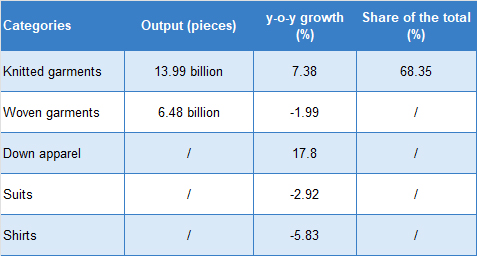

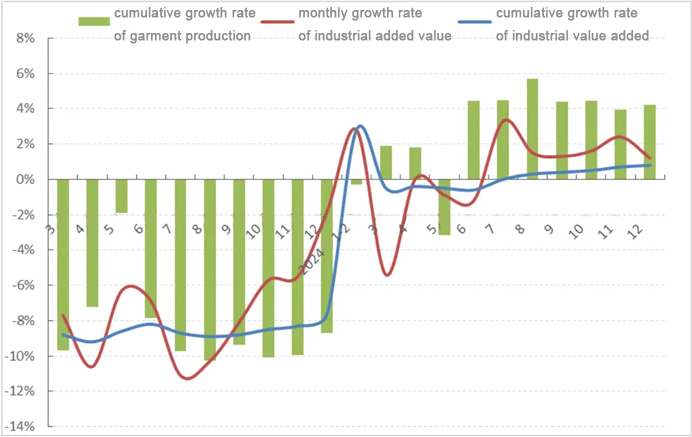

In 2024, China’s apparel production rebounded steadily, driven by the recovery of domestic and international market demand and product structure adjustment. According to the data from the National Bureau of Statistics, the industrial added value of apparel enterprises above designated size increased by 0.8% year-on-year in 2024, 0.4 percentage points higher than that of the first three quarters of 2024, and lifted by 8.4 percentage points compared with the same period of 2023. The apparel output of enterprises above designated size reached 20.46 billion pieces, up by 4.22% year-on-year, 0.19 percentage points lower compared with the first three quarters of 2024, but surged by 12.91 percentage points compared with the same period of 2023.

Table 1: Output of Major Apparel Categories in 2024

Figure 1: Production Growth Rate of China’s Apparel Industry in 2024

Source: National Bureau of Statistics

02. Domestic sales

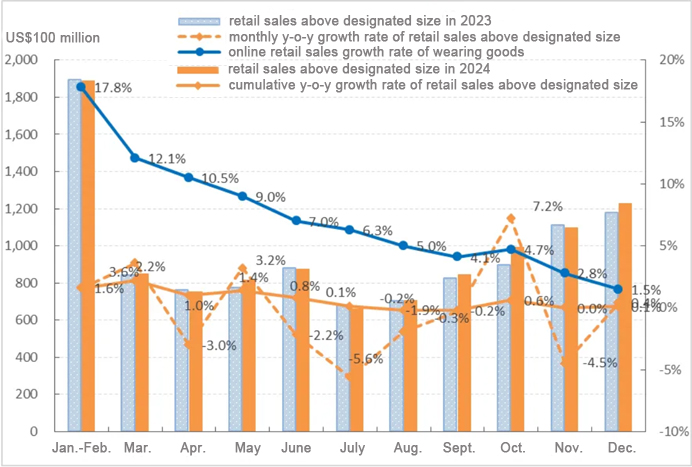

In 2024, the domestic apparel sales market maintained growth, supported by factors such as the gradual effect of national policies to promote consumption and the market vitality stimulated by new types of consumption and new modes of business. However, due to an insufficient willingness to consume and intensified competition in the market, the endogenous impetus of consumption was insufficient, therefore, the growth rate of domestic sales slowed down. According to the National Bureau of Statistics, China’s retail sales of apparel above designated size totaled 1.07 trillion yuan in 2024, seeing a year-on-year increase of 0.1%, 15.3 percentage points slower than that of the same period in 2023; online retail sales of wearable goods grew by 1.5% year-on-year, 9.3 percentage points slower than that of the same period in 2023.

Figure 2: China’s Apparel Sales in Domestic Market in 2024

Source: National Bureau of Statistics

03. Export

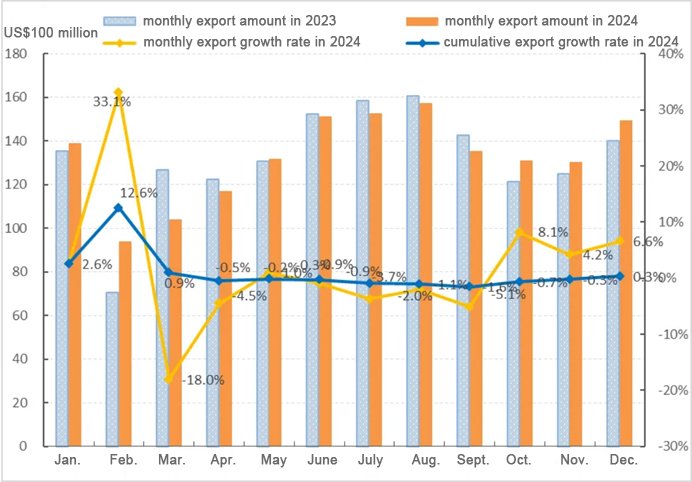

According to China Customs data, China’s cumulative exports of apparel and accessories totaled US$159.14 billion in 2024, up by 0.3% year-on-year, 8.1 percentage points higher than the same period in 2023. From the perspective of volume and price performance, apparel exports rose in volume and dropped in price. The apparel export volume reached 34.19 billion pieces, surging by 12.9% year-on-year. The average unit price was US$3.8 dollars per piece, declining by 11.2% year-on-year. Among them, knitted apparel exports amounted to US$71.23 billion, up by 3.8% year-on-year; its export volume increased by 12.5% year-on-year; the unit price fell by 7.7% year-on-year. As for woven apparel, its exports amounted to US$59.89 billion, seeing a year-on-year decline of 3.90%; the export volume surged by 13.6% year-on-year, and the unit price fell by 15.4% year-on-year.

Figure 3: China’s Exports of Apparel and Accessories in 2024

Source: China Customs

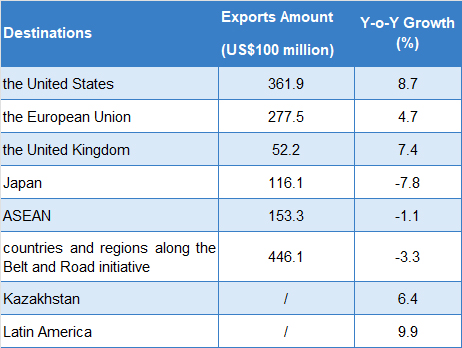

From the point of view of the major market, the apparel export market diversified. Benefiting from the better-than-expected economic growth in developed countries and the overall improvement in consumption, the international market demand has recovered. China’s apparel exports to the United States, the European Union and the United Kingdom grew, and the decline of that to Japan narrowed. During the same period, due to limited market space, coupled with last year’s high base factors, China’s exports to ASEAN, countries and regions along the Belt and Road initiative turned to negative growth, but the performance of exports to Kazakhstan and Latin America was brighter.

Table 2: China’s Apparel Exports by Destinations in 2024

Source: China Customs

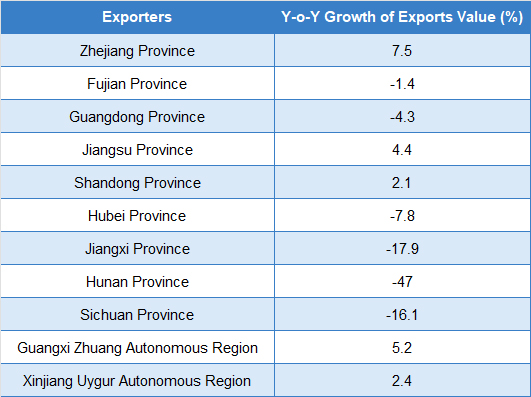

From the point of view of export provinces, the eastern region is still the major player in China’s apparel exports. The provinces in the central and western regions showed varied export performance; only Xinjiang Uygur Autonomous Region and Guangxi Zhuang Autonomous Region saw growth in exports.

Table 3: Apparel Exports Performance of China’s Major Exporters in 2024

Source: China Customs

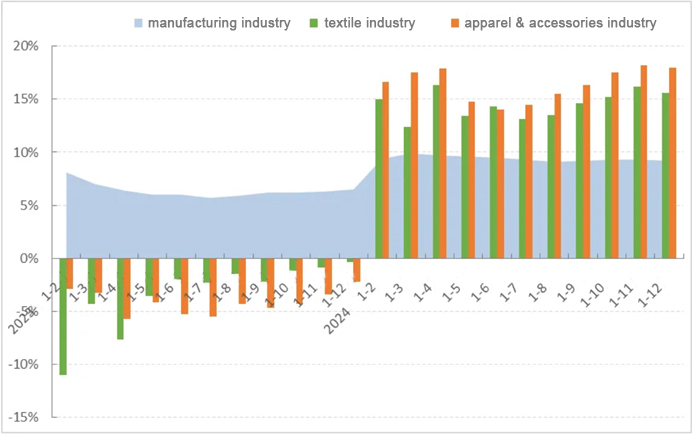

04. Investment

In 2024, apparel enterprises’ investment confidence gradually recovered, and the industry’s investment in fixed assets maintained relatively fast growth. According to the National Bureau of Statistics data, the investment in fixed assets in China’s garment industry in 2024 grew by 18.0% year-on-year, 20.2 percentage points higher over the same period of 2023, and higher than the overall level of the textile and manufacturing industries by 2.4 and 8.8 percentage points, respectively. Enterprise investment involves intelligent production, business model innovation, brand building, channel layout, and other areas to enhance supply chain management efficiency, optimize production processes, improve product quality, and reduce operating costs.

Figure 4: Fixed-asset Investment in China’s Textile Industry in 2024

Source: National Bureau of Statistics

05. Operation quality & efficiency

In 2024, China’s apparel industry made efforts to overcome difficulties and challenges such as insufficient consumer demand and intensified involutional competition. Supported by the continuous release of macro policy effects and accelerated development of new quality productivity, the industry realized restorative growth in operating income and total profit.

According to the National Bureau of Statistics, the main business income of apparel enterprises above the designated size totaled about CNY 1.27 trillion in 2024, with a year-on-year growth of 2.76, 8.16 percentage points higher than that of 2023. the total profit was CNY 62.38 billion, up by 1.54% year-on-year, 4.93 percentage points higher than that of 2023.

The margin rate of operating was 4.91%, 0.06 percentage points lower than in 2023 but 0.67 percentage points higher than the first three quarters of 2023. 20.07% of apparel enterprises above the designated size operated in deficit, 1.03 percentage points higher than that of 2023.

The turnover rate of finished products was 10.45 times/year, down 5.07% year-on-year; the turnover of accounts receivable was 6.26 times/year, seeing a year-on-year decline of 2.90%; and the total asset turnover was 1.16 times/year, down 0.30% year-on-year.

Figure 5: Main Economic Indicators of China’s Apparel Industry in 2024

Source: National Bureau of Statistics

II. Outlook for 2025

From the point of view of the international market, apparel exports will face increased downward pressure. The international market demand recovery momentum will be insufficient: the inventory replenishment cycle of Europe and the United States and other developed economies will come to an end; with geopolitical conflicts, trade protectionism and other uncertainties increased, will have a greater impact on China’s apparel exports. From the domestic market’s point of view, with the domestic economy picking up, consumer confidence and market vitality are gradually enhanced, and domestic demand is expected to improve. Coupled with the low base factor in 2024, the growth rate of domestic sales may rebound in 2025. Multiple positive factors will support the domestic sales of the apparel market to continue to rebound: First, policies such as expanding domestic demand, promoting consumption, and benefiting people’s livelihood, will enhance consumption capacity and consumer willingness. Second, the rise of new consumer groups represented by Generation Z and the new middle class promotes new consumption growth points such as sports, China chic, and sustainability. Combined with the new retail model of online and offline integration, consumption scenarios and consumption quality are innovating and upgrading. Third, the county market has shown great consumption potential and demand for consumption transformation. National brands and e-commerce platforms have accelerated the layout of the third-tier cities, releasing more apparel consumption demand.

Source: CHINA TEXTILE LEADER Express

Authority in Charge: China National Textile and Apparel Council (CNTAC)

Sponsor: China Textile Information Center (CTIC)

ISSN 1003-3025 CN11-1714/TS

© 2026 China Textile Leader, all rights reserved.

Powered by SeekRay